Shopping Cart

There are no more items in your cart

.png)

UHF RFID technology (860–960 MHz) enables the simultaneous reading of hundreds of tags at distances of up to 15 meters, with no line-of-sight requirement, where barcodes still demand manual, one-at-a-time scanning. It has established itself as the global standard for automated traceability across industries as diverse as logistics, retail, healthcare, and industrial asset management. Its key advantages include data accuracy exceeding 99%, an 80–90% reduction in cycle count time, and an ROI typically achieved within 12 to 18 months. Its only notable limitations involve sensitivity to metal surfaces and liquids, which require the use of On-Metal tags (also referred to as metal-mount RFID tags) in demanding industrial environments.

You need to print your own labels, but with the different printing technologies, roll sizes, compatible software, and types of ribbons, it’s often difficult to know where to start. No worries: by answering just a few simple questions, you’ll know exactly which label printer is right for you.

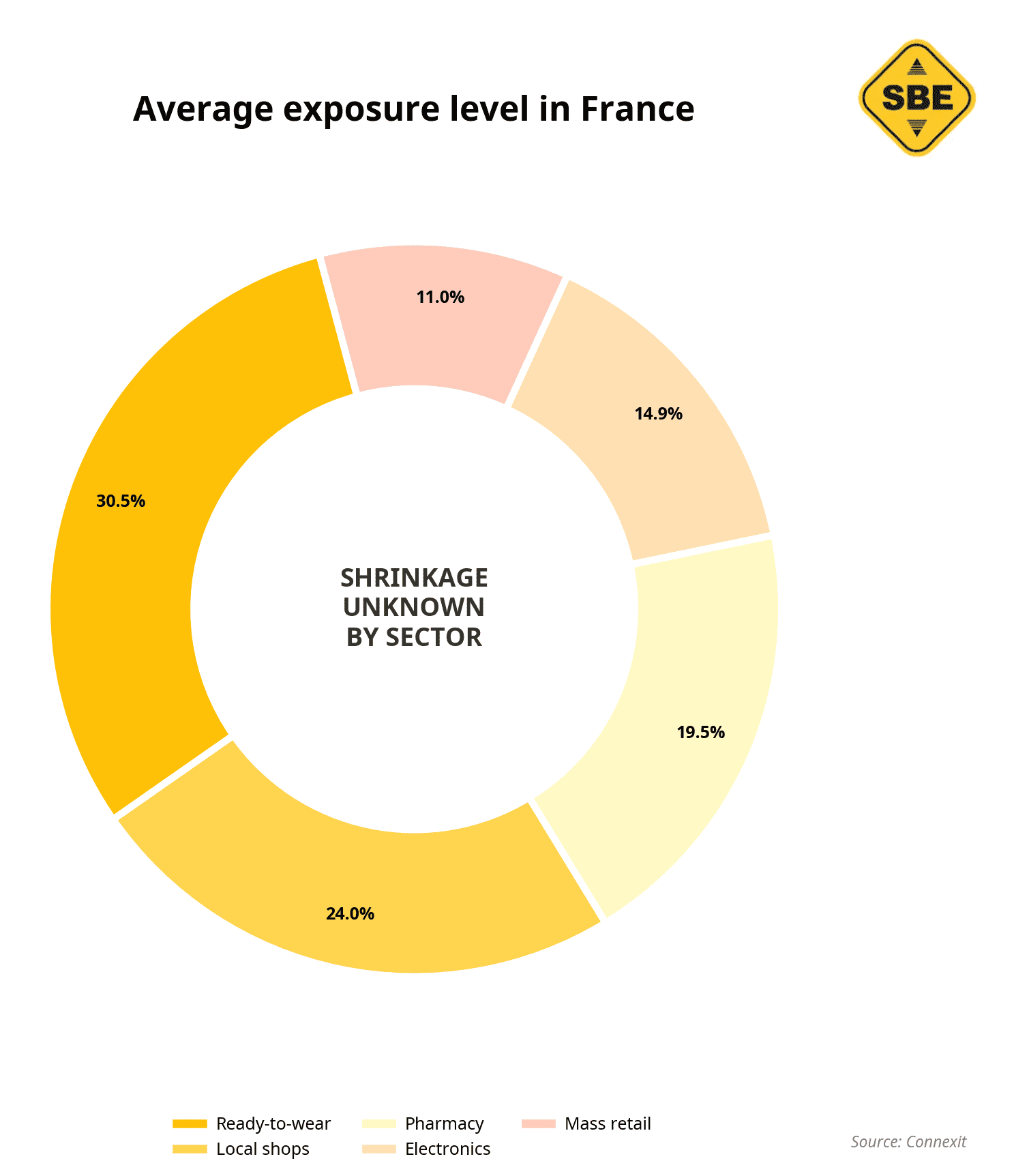

Tools, smartphones, alcohol, razor blades, jewellery and make-up are the products most coveted by thieves because of their high added value. Theft is a scourge for supermarkets and specialist retailers. It accounts for nearly 80% of "shrinkage", which represents all the goods that go missing, including stock management errors, supplier errors, breakage and waste. In Europe, France is one of the countries most affected by shrinkage with 6.5 billion euros lost, including more than 468 million euros for specialised distribution. It is mainly due to external/shoplifting (43%), internal/employee fraud (24%), suppliers (17.5%), then internal errors/administrative losses (16%). (source: 22/10/20, Stackr). To counter theft, it is therefore essential to invest in effective and reliable means such as anti-theft security labels. In this article, you will learn about the different types of anti-theft labels and their advantages.